Copyright © 2022 NC Media Pvt. Ltd. All Rights Reserved.

Fact Check

Does The Income Tax Act 2025 Allow Authorities Access To Everyone’s Digital Accounts?

Claim

The Income Tax Act 2025 gives tax authorities unrestricted access to people’s social media accounts, emails, and digital spaces to curb tax evasion.

Fact

The Act allows access to digital information only in specific, authorised cases and does not permit blanket or routine digital surveillance.

The Income Tax Act 2025, which replaces its predecessor, the Income Tax Act 1961, was passed in August 2025 and will come into effect from April 1, 2026. Ahead of its implementation, several social media users claimed that the newly introduced law gives Income Tax authorities a free pass to access social media accounts, emails, and other digital spaces of individuals to curb tax evasion. The claim has raised concerns around digital privacy.

Also Read: Old, Unrelated Videos Shared To Show Massive ‘Save Aravalli’ Protest In Rajasthan

Evidence

What the Law Says?

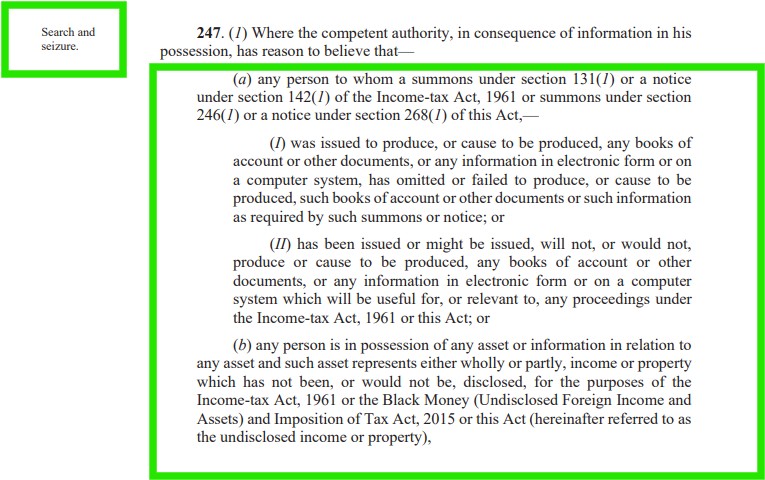

Newschecker accessed the new legislation and began its investigation by closely examining its provisions. Section 247 of the Income Tax Act, 2025 specifically deals with “Search and Seizure.”

Section 247(1) states that search and seizure powers can be exercised only when the competent authority, based on information in its possession, has reason to believe that a person has either failed to produce required books of account, documents, or electronic records despite being issued a summons or notice, or is likely to withhold such material even if a summons or notice is issued, provided the information is relevant to proceedings under the Income Tax laws.

The provision also applies where a person is in possession of an asset, or information relating to an asset, that represents wholly or partly undisclosed income or property under the Income Tax Act, 1961, the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, or the new Act.

In such cases, the approving authority may authorise an officer to take the following actions:

“(i) enter and search any building, place, vessel, vehicle, aircraft where he has reason to suspect that such assets, books of account or other documents, or such information in electronic form or on a computer system are kept;

(ii) require any person, who is found to be in possession or control of any books of account or other documents maintained in the form of electronic record or any information in electronic form or on a computer system, to afford the authorised officer with such reasonable technical and other assistance (including access code, by whatever name called) as may be necessary to enable the authorised officer to inspect such books of account or other documents or such information;

(iii) break open the lock of any door, box, locker, safe, almirah, or other receptacle or override the access code to any computer system for exercising the powers conferred by clause (i) where the keys thereof are, or the access to such building, place, etc., or the access code to such computer system, as the case may be, is not available;

(iv) search any person who has got out of, or is about to get into, or is in, the building, place, vessel, vehicle or aircraft, if the authorised officer has reason to suspect that such person has secreted about his person any such books of account, other documents, any information in electronic form, or a computer systems or asset;

(v) place marks of identification on any books of account or other documents, or make or cause to be made extracts or copies therefrom and also from computer system;

(vi) make a note or an inventory of any such asset, and stock-in-trade of the business, found as a result of such search;

(vii) seize any such books of account, other documents, computer systems or asset (other than stock-in-trade of the business), found as a result of such search,” the law states.

No Provision for Blanket Digital Surveillance

A plain reading of Section 247 shows that access to electronic information, including computer systems, is permitted only during formally authorised search and seizure operations. These powers are conditional and triggered only when authorities have recorded reasons to believe that tax violations involving undisclosed income or assets have occurred. The provision does not allow general or routine monitoring of digital activity of the public.

‘Search & Seizure’ Existed Under the 1961 Act

It is also notable that search and seizure powers are not entirely new. Similar provisions existed under Section 132 of the Income Tax Act, 1961, which allowed searches and seizures under defined circumstances. However, the scope of such powers has been expanded in the new law to include digital spaces such as electronic records and computer systems.

Expert Clarification

Newschecker reached out to Shankey Agrawal, Partner at BMR Legal, who clarified:

“The new income tax law does not permit an open-ended or routine digital surveillance of emails or social media accounts. Such access is permissible only in the context of a formally authorised search and seizure proceedings.

That said, if a valid reassessment notice is issued to an individual or entity, officials may examine relevant information including access to social media accounts as part of that process.”

Income Tax Department’s Statement

The Income Tax Department itself addressed the concern in a recent post, stating:

“The provisions of section 247 of the Income Tax Act 2025 are strictly limited to Search and Survey operations. Unless a taxpayer is undergoing a formal search operation due to evidence of significant tax evasion, the department has no power to access their private digital spaces.

The powers cannot be used for routine information gathering/processing, or even for cases under scrutiny assessment. These measures are specifically designed to target black money and large-scale evasion during search and survey, not the everyday law-abiding citizen.”

Verdict

Social media posts claiming that the Income Tax Act 2025 allows unrestricted access to emails, social media accounts, and digital spaces leave out crucial legal context. While the law does expand search and seizure powers to include electronic records, these powers are tightly linked to specific, authorised proceedings and cannot be exercised arbitrarily.

FAQs

Q1. When does the Income Tax Act 2025 come into effect?

The Act will come into force on April 1, 2026.

Q2. Which section of the new law deals with digital access during searches?

Section 247 of the Income Tax Act 2025 governs search and seizure, including access to electronic records.

Q3. Did similar search powers exist earlier?

Yes. Similar provisions existed under Section 132 of the Income Tax Act, 1961, though the scope has now been expanded to cover digital records.

Sources

The Income Tax Act, 2025

Facebook Post By Income Tax India, Dated December 22, 2025

Conversation With Shankey Agrawal, Partner At BMR Legal On December 27, 2025

RESULT Missing Context

Missing Context

Missing ContextData PrivacyDigital SurveillanceFact CheckIncome TaxIncome Tax Act 1961Income Tax Act 2025Income Tax Department

If you would like us to fact check a claim, give feedback or lodge a complaint WhatsApp us at +91-9999499044 or email us at checkthis@newschecker.in. You can also visit the Contact Us page and fill the form.